Pharmacies are the place to sell Beauty in France

The CEW France held its Beauty Business Day recently, and we caught up with the latest in Beauty.

From Nielsen IQ (Global Beauty France), to Circana (Mass & Prestige), to OpenHealth (pharmacies), the figures reveal a changing landscape in beauty retail. Expert-based beauty advice, AKA pharmacists, seems to be the winning factor in the French landscape.

Is this trend only relevant to the French market, or is it indicative of a global trend toward more curated beauty purchases? With the plethora of beauty products on the market, chances are that consumers are as lost as we are as beauty professionals, and may need guidance, and who has a better voice than a valued pharmacist?

You can access the replay (in French), here.

The French Pharmacy, the epicentre of holistic beauty

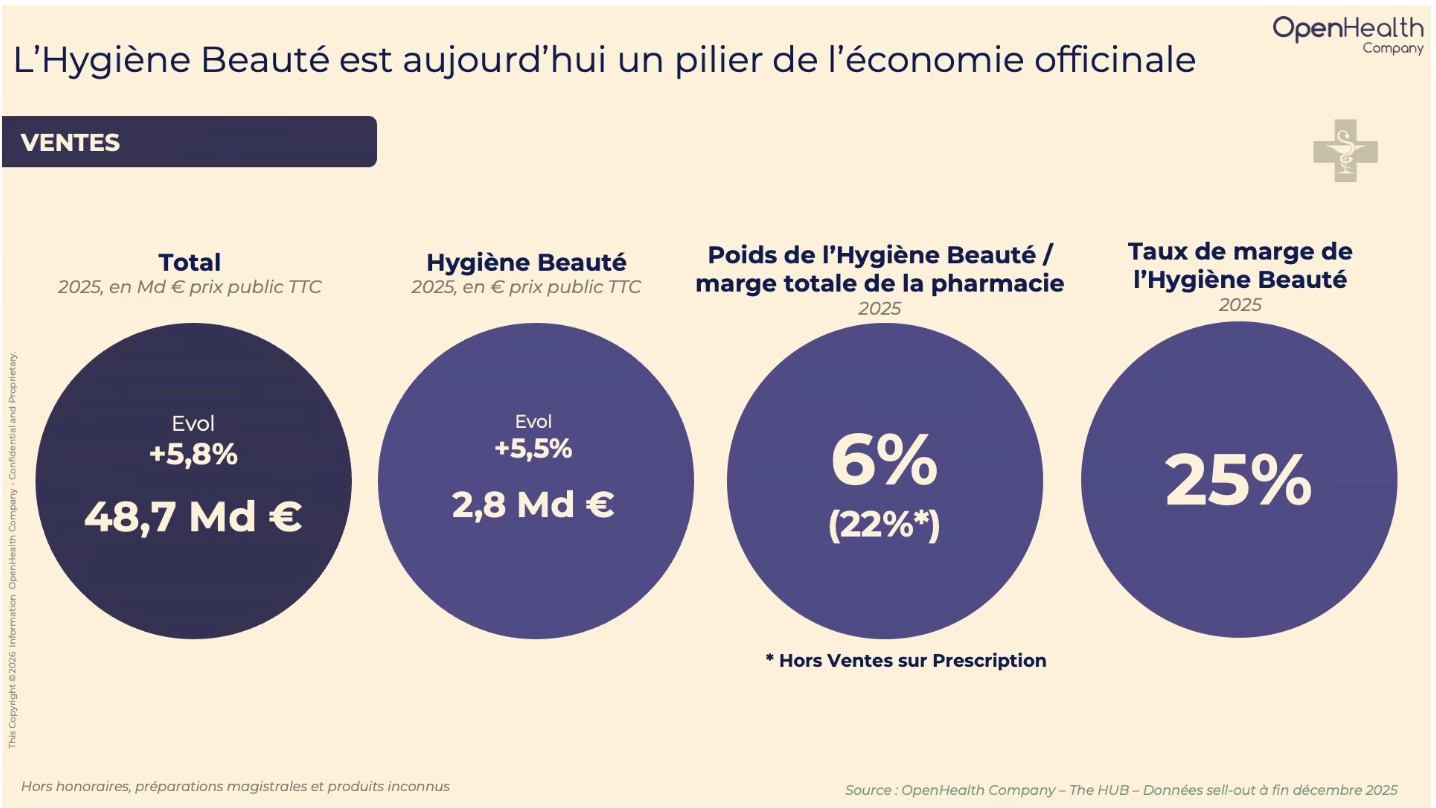

According to OpenHealth, the hygiene and beauty segment has grown on average by 8% over the last 4 years (2021-2025) - compared to a 3% annual average growth over the previous 4 years - and is expected to continue on its trajectory. Pharmacies are becoming the centre of health, where professional advice turns into beauty sales.

On a side note, in France, beauty brands can often offer a reward system to staff at pharmacies who receive special offers in exchange for being identified as “brand ambassadors” within the pharmacy. It’s a win-win for the brand that gains a credible expert, the customer who receives tailored advice, and the employee who takes on a special responsibility.

The French market comprises 304 XXL pharmacies with an annual turnover of about or over 7 Million €, 1,501 advice pharmacies with a turnover between 4 and 7 Million €, and 17,765 local pharmacies with a turnover of 4 Million euros or under. The Hygiene and Beauty segment represents 6% of pharmacies' margin, but it offers a margin rate of about 25%, which is higher than other segments, which could be an incentive for pharmacists.

But pharmacies are a tough territory to penetrate because it requires sales staff to roam the country to reach each pharmacy and speak with pharmacists. Proof that technology has a long way to go, and that people still need connection, and pharmacies offer just that. Recent entrants like La Rosée (sold in about 10,000 pharmacies) and Krème (sold in about 2,500 pharmacies) have gained national visibility, thanks to their know-how as both brands' founders came from the circuit. No coincidence here, yet, smart strategy and seamless execution.

The pharmacy will keep growing as medical services are transferred from medical practices to local pharmacies to support rural life, where doctors are becoming scarce and pharmacies play a central role in local life, or where the French national healthcare system is offloading small tasks to pharmacies (vaccination, testing, etc.).

Other Beauty Channels

Nielsen IQ revealed global market figures. Only 17% of consumers feel they can spend freely, and FMCG beauty has seen a 0.2% decrease in 2025, and purchase intentions are decreasing for about a quarter of consumers globally.

Skin care and perfume drive growth; online beauty outperforms; and sometimes it is the only retail channel that grows. Globally, 4 people out of 10 bought Beauty on Amazon, especially men. Vinted is now the number 4 online retailer globally, and TikTok is number 2 in the UK and number 6 in the US, and number 5 in the US, whereas in France it is number 34, demonstrating scepticism of the platform in the French market. A note: generative AI is becoming a beauty advisor for beauty consumers.

On other figures, Nielsen revealed that 52% are ready to pay more for products that make tasks easier / less time-consuming, and consumers are looking for a more wellness- and holistic-oriented approach, with beauty treatments and supplements showing increased interest. Another note: K-beauty has grown by 54% in France over the last year and has doubled in value since 2023.

As for Circana’s figures in beauty retailers (except online), they revealed that the selective perfumery segment decreased by 1,3% and the mass market by -1,6%, and pharmacies grew by 6%.

Circana revealed that mono-brand retailers perform very well, with an average growth rate of about 21%. Chinese retailers like Temu and Shein grew by 12%, while discount stores like Normal and Action grew by 15%.

The Circana report also demonstrates consumer interest in more sustainable options, with 58% prioritising products made locally (in France), 36% prioritising “without,” and 31% prioritising “eco-design”.

The figures speak for themselves

What do the figures tell us about the state of beauty in France? Overall, the last figure from Circana showed that France was the only country to decrease by 1% in the prestige beauty segment, while the overall market grew by an average of 10% in the segment.

Pharmacy is a key driver of growth and comes with specialist advice for beauty. Prestige beauty has seen a decline in France, linked to overall inflation, which was the highest in Europe compared to neighbouring countries.

Price is the key driver for growth in the mass market, and service is one in selective or specialist retailers.

Just a note for the editor

Pharmacies may be the key to more sustainable behaviour, since testimonials from beauty professionals indicate that sustainable purchases are often higher when a beauty adviser supports a more conscious purchase. For instance, Circana found that bigger formats sell well in pharmacies and are also often pushed by staff.